ICICI Smart Assistant

ICICI Smart Assistant

_RGB.png)

NRIs returning to India: An essential financial guide

Read time: 11 mins

Share

-

Know the banking and financial to-dos for NRIs once they relocate to India

-

Understand your new residency status and the associated tax implications

The below content is purely for informational purposes and is not intended to constitute advisory of any kind. Please note, these are in-depth articles which are best viewed on large screen devices like laptops, desktops and tablets. The position reflected in this article has been updated as of February 15, 2024.

A shift back to your home country carries mixed emotions of apprehension and excitement. If you are a Non-Resident Indian (NRI) planning to move back to India, we have listed a few tips that will facilitate a quick and seamless transition.

1. Relocated back to India? Banking to-dos for NRIs

As an NRI, you may have various bank accounts in India, such as Non-Resident Ordinary (NRO), Non-Resident External (NRE), Foreign Currency Non-Resident Bank (FCNR(B)), or international bank accounts. It is important to understand what happens to these accounts when you relocate to India.

a. Revisit your bank accounts held in India

As per the Reserve Bank of India (RBI), on permanent relocation to India, you cannot continue to hold your NRO/NRE bank accounts. Let us look at the options available to you for these accounts.

- NRO account: You need to mandatorily convert your NRO account to a resident savings account or close the account.

- NRE account: You need to mandatorily convert your NRE account to a resident savings account or transfer the funds held in your NRE account to a Resident Foreign Currency (RFC) account.

Did you know?

A RFC account is an Indian bank account maintained in foreign currency that allows returning NRIs to park their foreign earnings. There is no repatriation limit on funds held in your RFC accounts. In case you become an NRI again, you can transfer the funds held in this account to an NRE/FCNR (B) account.

- FCNR (B) account: You can hold your FCNR (B) fixed deposits until maturity. After that, you will need to transfer its proceeds into a resident savings account (maintained in Indian rupees) or an RFC account. (if you want to keep holding the foreign currency.)

b. Evaluate usage of your international bank accounts

As per the Reserve Bank of India (RBI), you can continue to hold your international bank accounts, which you had opened overseas when you were an NRI. However, you may need to ascertain whether the regulations of the country, where you hold the account allows you to continue maintaining these accounts.

2. Managing your existing investments

As you transition to a new residency status in India, you should review and assess the implications of the same on your existing investments in India and overseas.

a. Investments in India

- Demat account: You should inform the bank and broker about your new residency status. You will have to open a new resident demat account and have your existing securities held in your NRI demat account transferred to this account. Subsequently, you will then also have to close your NRI demat account and the NRE Portfolio Investment Scheme (PINS) account. In addition, you will have to do a fresh Know Your Customer (KYC) and update your Foreign Account Tax Compliance Act (FATCA) declaration as applicable for the United States (US) or Common Reporting Standard (CRS) for the United Kingdom (UK), Canada or any of the 100+ countries that have adopted CRS.

- Mutual funds: You must inform your bank/broker/Asset Management Company (AMC) through whom you have invested in mutual funds about the change in your residency status, and have your linked NRI bank accounts updated to a resident savings accounts. You will also have to update your KYC and FATCA/CRS status.

- Fixed deposit (FD): If you have an FD account, such as an NRE/NRO FD, the account should be converted to a resident FD account. You will still earn interest and the same will be taxable at the applicable tax rates.

b. Investment in overseas assets

As per the prevailing Foreign Exchange Management Act (FEMA) regulations, you are permitted to continue holding your overseas assets (which you had invested in when you were an NRI) when you become a resident Indian. You must check with your current country of residence if you can hold these assets once you move to India.

3. Insurance policies

NRIs returning to India can continue with their insurance policies (e.g., health insurance, motor insurance etc.) purchased in India, as long as they continue with the said policy while they were designated as NRIs. Life insurance policies purchased from India, should be valid upon your return, provided you have paid all due premiums. You must notify the insurer of your change in residential status and update your bank account information. Submission of the request documents will also be necessary for a seamless process. The insurance policies you purchase in a foreign country may not be valid once you return India.

Once you return to India as a resident Indian, you have all investment options available including those which were previously restricted for you as an NRI. These include - opening a new Public Provident Fund (PPF) account, investing in Tier II National Pension Scheme (NPS), all types of mutual funds, intraday trading in stocks, Sovereign Gold Bonds (SGBs), agricultural land, plantation, trading in currency derivatives and commodities, RBI floating rate savings bond etc. You should get in touch with your bank or investment advisor for more details.

Tax implications when you return to India

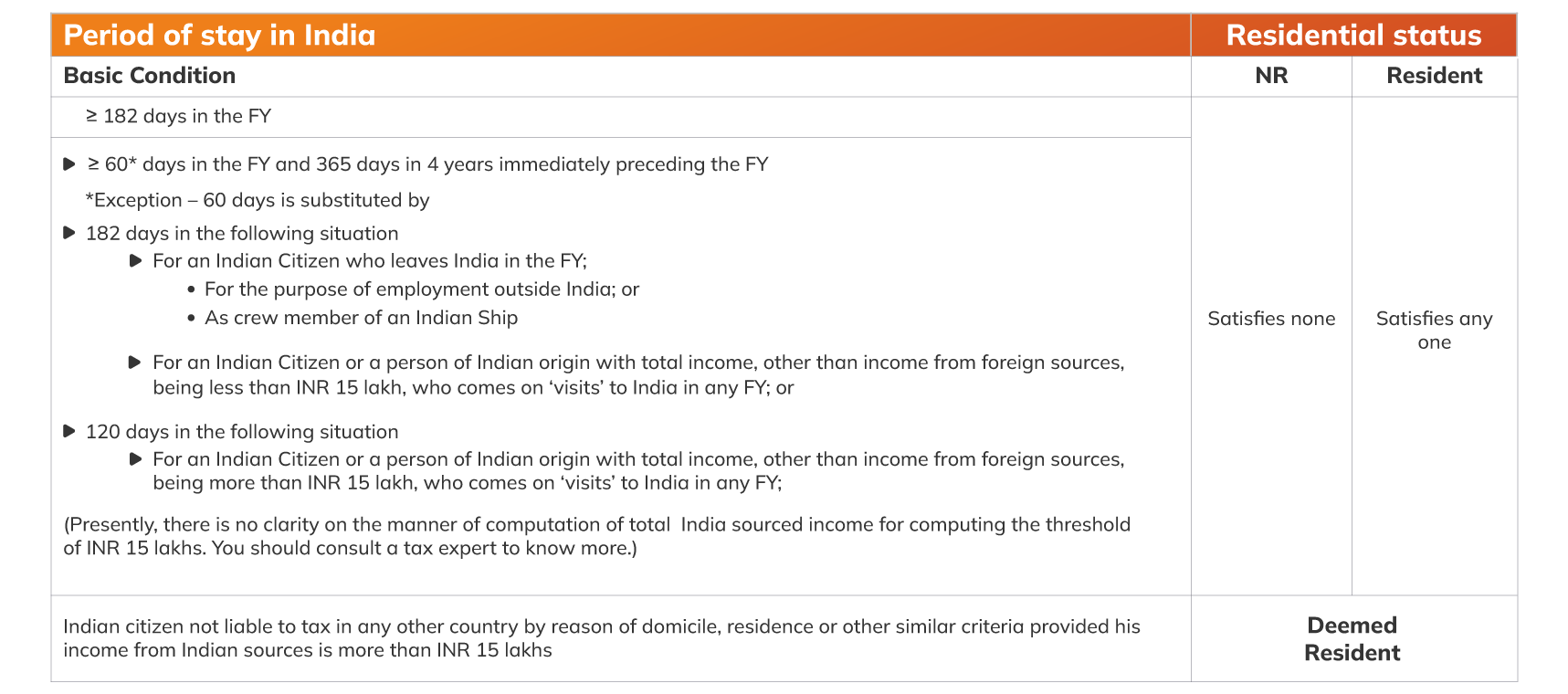

When you return to India, your residency status will undergo a change. You will qualify to become a ‘resident’ in any Financial Year (April - March) if you satisfy any one of the conditions outlined in the table below:

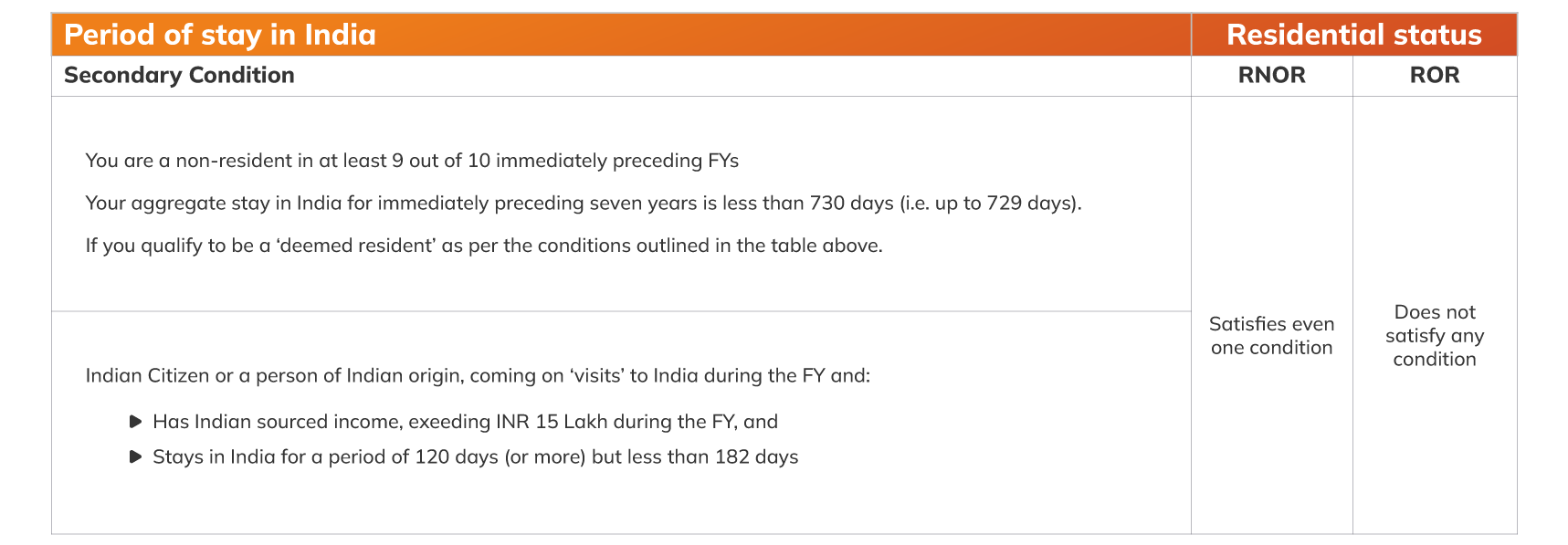

Based on the above residency conditions, once you qualify as a ‘resident’ on your return to India, you may be considered either a Resident and Ordinarily Resident (ROR or OR), or Resident but Not Ordinarily Resident (RNOR or NOR) based on the below conditions:

Generally, over a period of two to three FYs, you will transition from being an RNOR to an ROR. Sameer, an Indian citizen, left India for the first time and went to the United States (US) for employment purposes in January 2012. He returned to India permanently on August 1, 2022. Let’s understand how his residency status will change over the next few FYs.

- FY 2022-23: He will qualify as a resident because his stay in India exceeds 182 days during the FY. Further, as a resident, he will qualify as an RNOR since:

- He is not a resident for at least 9 out of 10 immediately preceding FYs; and

- His cumulative stay during the immediately preceding 7 years is less than 730 days.

- In FY 2023-24: He qualifies to be a resident. Although, he has not been a non-resident in at least 9 out of 10 immediately preceding FYs, he will still qualify as an RNOR because his cumulative stay has not yet exceeded 729 days during the preceding 7 years.

- In FY 2024-25: He will qualify as an ROR as:

- He has spent more than 182 days in India in the financial year.

- His cumulative stay in India during the immediately preceding 7 years is more than 730 days; and

- He has not been a non-resident in at least 9 out of the 10 years preceding FY 2024-25.

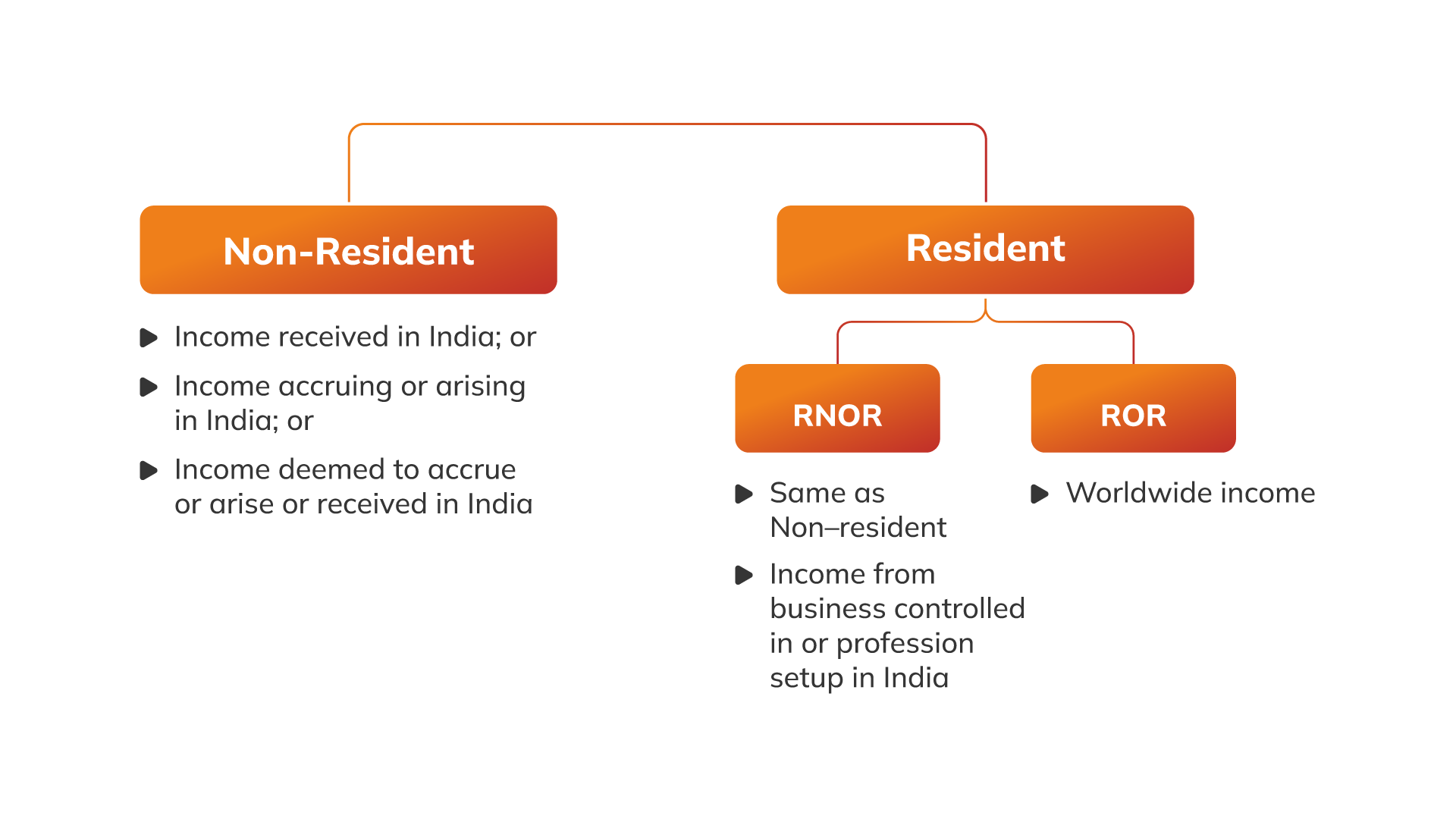

Your taxability depends on whether you qualify to be an RNOR or an ROR. You can determine your taxability as per the table outlined below:

Please note, tables are best viewed on desktops and in landscape mode on mobile phones.

| Particulars | Non-Resident (NR) | RNOR | ROR |

|---|---|---|---|

Income accruing or arising, or which is deemed to accrue or arise in India. |

Taxable |

Taxable |

Taxable |

Income received or is deemed to be received in India. |

Taxable |

Taxable |

Taxable |

Income accrues or arises outside of India. |

Non taxable |

Non taxable |

Taxable |

The key difference between the taxability of an RNOR and a non-resident is that income earned outside India will be subject to taxation for an RNOR only when it is derived from a business or profession that is controlled from India. On the other hand, NRIs are not liable to pay tax on such income.

Sameer continues to earn foreign income from his investments abroad. In FY23 and FY24, since he qualifies to be an RNOR, he will not be liable to pay tax on his foreign income in India. Here are some examples of foreign income on which he will not be liable to pay taxes in India:

- Rental income received in a foreign bank from a property situated abroad.

- Dividend or interest received in foreign banks from foreign shares and securities.

- Withdrawals from offshore retirement accounts.

- Gains derived from capital assets situated abroad.

- Interest earned on RFC and FCNR (B) accounts.

Starting in FY25, once Sameer attains ROR status, his foreign income will become taxable in India. However, if any of his foreign income is subject to double taxation, he will be eligible to claim benefits under the Double Taxation Avoidance Agreement (DTAA) between India and the country where the income originated.

Click here to learn more about DTAA.

Your tax rates will be as per the prevailing income tax laws in India. You should consult a tax expert to determine your tax liability and understand the income tax rules for NRIs returning to India.

Conclusion

NRIs returning to India should proactively manage their banking and investment affairs to ensure compliance with Indian regulations. You should promptly notify the change in your residency status to your bank, broker, AMC, and insurance service providers. You will need to convert your NRE, NRO accounts to resident savings accounts, and close NRI demat accounts. The tax implications on your existing investments will change as per your residency status. You should get in touch with your bank or a tax expert to know more details.

This is sample bottom text

Recommended For You

-help-an-nri-oci-pio.webp)

Disclaimer:

The contents of this article/infographic are meant solely for informational purposes. The contents are generic in nature and are not intended to serve as a substitute for specific advice on any matter whatsoever. The information is subject to updation, completion and verification and the applicable norms may keep changing materially from time to time. This information is also not intended for distribution or use by any person in any jurisdiction where such distribution or use would be contrary to applicable laws or would subject ICICI Bank Limited/its affiliates to any licensing or registration requirements. ICICI Bank Limited/its affiliates and their representatives shall not be liable for any direct or indirect losses or liability incurred arising in connection with any decision taken by any person on the basis of this content. Please conduct your own due diligence and consult your financial advisor before making any decision. Terms and conditions of ICICI Bank and third parties apply. ICICI Bank is not responsible for third party services. Nothing contained herein shall constitute or be deemed to constitute an advice, invitation or solicitation to avail any products/ services of third parties.